You have built the business case. The value hypothesis is defensible, the cost model is complete, the risk register is honest, the financial model is finance-grade. Now you have to present it.

The presentation is not a small step. I have watched excellent business cases die because they were presented badly, and I have watched weaker cases get approved because the presenter understood what the CFO actually wanted to hear. Understanding the room, structuring for it, and handling the hard questions well are separate skills from building the case itself, and this article is about them.

What CFOs actually want to see

CFOs read hundreds of business cases in a year. The ones that stand out are the ones that respect their time and their scepticism. Three things matter most.

The first is the bottom line up front. The CFO wants to know, in the first 30 seconds, what you are asking for, what you expect back, and when. Every additional slide before that answer erodes their patience. If your deck opens with “First, some context on AI adoption,” you have already lost the room.

The second is honest treatment of risk. CFOs have been burned by too many technology investments that were presented as sure things and turned out not to be. A case that opens by acknowledging the top three risks and explaining the mitigations reads as competent. A case that hides risks in the appendix reads as evasive.

The third is credible attribution. Where do the numbers come from, how reliable are they, what could invalidate them? A case with sourced assumptions and confidence ranges is much more persuasive than a case with confident-sounding numbers and no provenance.

Boards care about a slightly different set of things. They want strategic narrative on top of financial rigour, competitive context, and enough understanding of the risk profile to fulfil their fiduciary responsibility. Board presentations need everything the CFO presentation needs, plus a layer of strategic framing that ties the investment to enterprise-level bets and market position.

The one-page structure that works

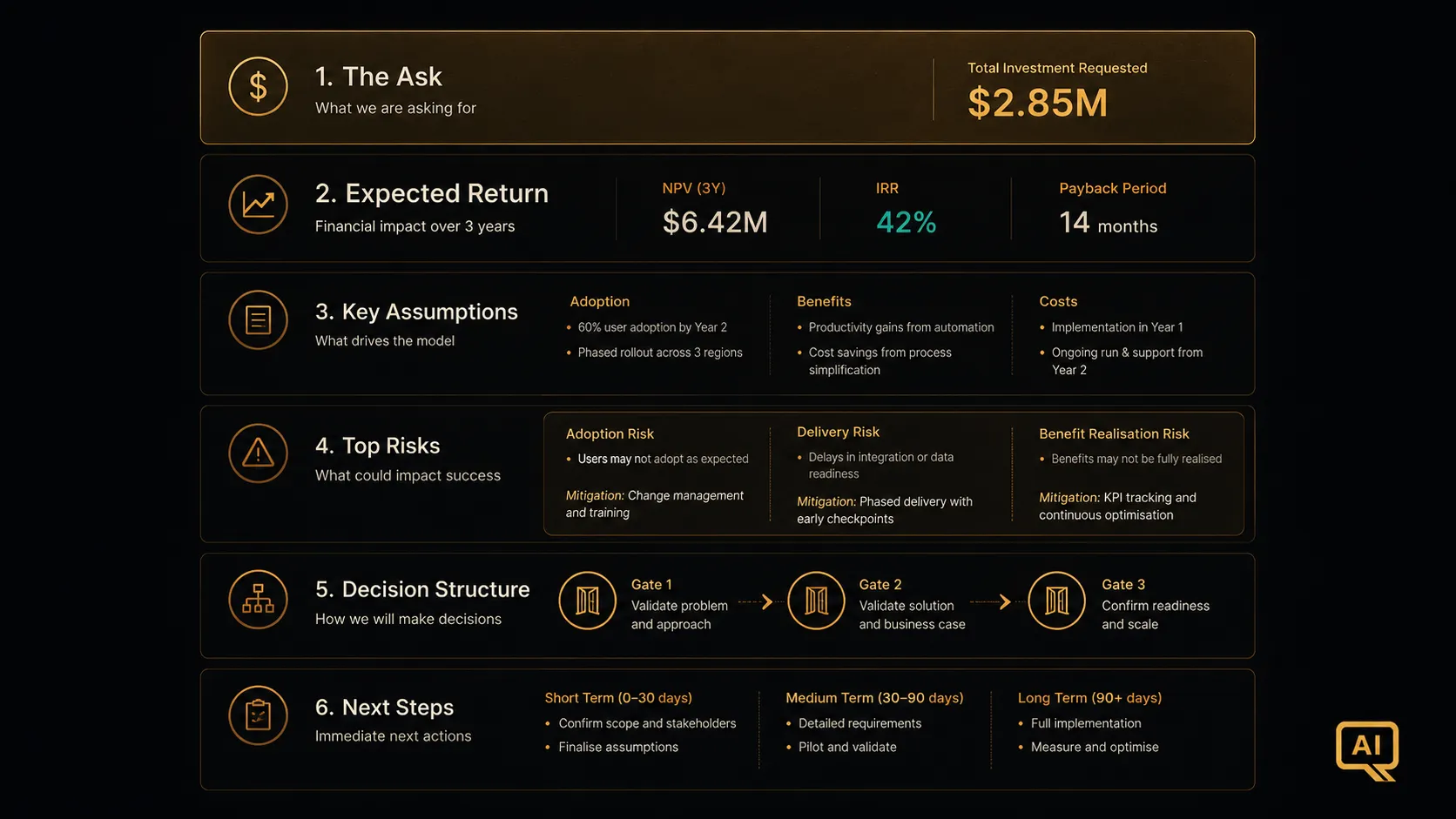

Figure 1 shows the one-page structure I have found works best for AI business cases going to a CFO or board. It has six sections, each with a specific job.

Section one at the top of Figure 1 is the ask. Concrete, specific, dollar-amount, timeframe. “Approve $4.2M investment over 18 months to deploy a customer support AI copilot to 850 agents.” Not “AI transformation initiative.” Not “customer experience enhancement.” The specific ask.

Section two is the expected return. Three-year NPV, IRR, payback period, all in a single line. If your case runs multiple scenarios, show base case as the headline number and reference the range.

Section three is the top three assumptions the case depends on. Adoption rate, per-task value, cost trajectory. The reader should be able to see what has to be true for the numbers to hold.

Section four is the top three risks. Not exhaustive; the three that would most materially affect the outcome. Each with its mitigation approach.

Section five is the decision structure: staged investment with go/no-go gates, and what evidence would trigger continuation, hold, or exit at each gate. This is the real options thinking from BCR-08 rendered for the boardroom.

Section six is next steps: what you are asking the CFO to do specifically (approve stage one, set a review date, delegate ongoing governance to a specific committee).

A CFO can read this in 90 seconds and know whether to engage further or ask for changes. The rest of the deck exists to answer the specific questions they will have after reading it.

Capex versus opex classification

This is the accounting question that comes up in every AI business case, and getting it wrong causes real problems.

Traditional software historically fell into capex: capitalise the implementation cost, amortise over useful life, take periodic impairment reviews. Cloud infrastructure and SaaS moved most software spend to opex: expensed as incurred, no capitalisation.

AI spend is largely opex. Model licences, token spend, platform team salaries, ongoing training and change management: all opex. This has two implications the business case needs to address.

First, opex spend hits the current-year P&L directly, which can be a hard sell if the company is under earnings pressure. Cases that are objectively good NPV can be politically difficult because the year-one hit is large and visible.

Second, opex spend is not on the balance sheet, which affects certain financial ratios and covenants. This rarely kills a case but it can affect timing and structuring.

The workaround some organisations use is to capitalise the initial build costs (integration work, custom development, initial infrastructure setup) as internally developed software, while keeping ongoing operating costs as opex. This is a legitimate accounting treatment when the criteria are met, and it can materially change the P&L presentation. Discuss it with your finance controller before the presentation, not during.

Framing risk for the board

Boards think about risk differently from operators. Operators think in terms of specific things that could go wrong; boards think in terms of exposure levels the organisation can tolerate. The framing has to reflect both.

For an AI investment, the risks that matter to the board typically fall into five categories.

Financial exposure: what is the maximum downside, and can the organisation absorb it without material impact? Framing your case in staged investment terms (BCR-08) makes this easier to answer, because the maximum downside at any point is bounded by the current stage commitment.

Reputational exposure: what is the visible failure mode if the AI produces a bad output at the wrong moment? For customer-facing deployments this is often the risk that keeps boards up at night, and the mitigation (human review, staged rollout, kill switches) needs to be explicit.

Regulatory exposure: what happens if regulation changes in ways that restrict the deployment? The EU AI Act (fully enforceable August 2026), state-level rules in the US, and sector-specific regimes are all active concerns.

Competitive exposure: what happens if we do not invest? The 21 percent of S&P 500 companies who can cite measurable AI benefit are pulling ahead of the 79 percent who cannot. This is not a reason to invest badly, but it is a reason to invest, and the board should understand the counterfactual.

Vendor concentration exposure: what is our reliance on any single AI provider, and how do we manage the risk if they change pricing or capability? Multi-model architecture is not just a cost lever; it is a risk management posture.

The three hard questions to prepare for

Every AI business case presentation gets three questions I have seen almost universally. Preparing specific answers to them is not optional.

“What about the 95 percent failure statistic?” The MIT NANDA finding is now common knowledge, and any CFO or board member with basic awareness will raise it. The answer is not to dispute the statistic; it is to explain how your specific programme structure addresses the specific reasons those failures occurred. Deliberate rollout design, measurement instrumentation from day one, adoption planning, workflow redesign: these are the differences between the 5 percent who succeed and the 95 percent who do not. The case should show that you have all of them.

“How do we know the vendor will still be around in three years?” AI vendor market dynamics are unsettled, and this concern is legitimate. The answer includes vendor financial due diligence (is the vendor well-funded, is the underlying business viable), architectural resilience (multi-model deployment, workload portability), and staged commitment (contracts structured to allow exit at reasonable points).

“Why now?” The competing case for AI investments is often that waiting a year would be cheaper (models better, costs lower, patterns clearer). This is sometimes a genuine question and sometimes a delay tactic. The answer depends on your specific situation, but it usually involves competitive dynamics, adoption learning curves, and the value of building organisational capability that compounds over time. Not every AI investment has to be made now; the case should show why yours does.

The presentation flow

Figure 2 shows the presentation flow for a typical 30-minute CFO conversation. The times are approximate, but the sequence matters.

Minutes 0 to 2: the ask and the headline return. This is the anchor. Everything after this either supports or refines it.

Minutes 2 to 8: the value case. How do we get the return, what does the mechanism look like, what evidence do we have that the mechanism will work in our organisation.

Minutes 8 to 15: the cost case. Full stack, honest projection, sensitivity analysis. This is where you demonstrate that you have thought about the surround, not just the vendor invoice.

Minutes 15 to 22: risks and mitigations. Structured around the five categories above. Explicit about what could go wrong and what the response is.

Minutes 22 to 27: the decision structure. Staged investment, gates, evidence required at each stage. This is where you show the CFO that you are not asking for the whole commitment upfront, and that the ongoing decision to continue is anchored in real evidence.

Minutes 27 to 30: the ask again, and next steps. Close the loop.

The flow in Figure 2 assumes a 30-minute slot. For board presentations, the sequence is the same but compressed, with more time on the strategic framing at the top and less time on operational detail. For deeper working sessions with finance, the flow is inverted: cost model and financial detail get the bulk of the time.

What to leave in the appendix

The main deck should not exceed 15 slides for a CFO conversation, 10 for a board. Everything else goes in the appendix, and the appendix should be organised so specific questions can be answered by turning to specific sections.

The appendix belongs the detailed financial model, the full sensitivity analysis, the vendor comparison, the technical architecture summary, the risk register in full, the change management plan, the measurement plan, the sample dashboard, and the reference customer case studies. All of it should be at hand, but none of it should be in the primary flow unless a question specifically raises it.

The mistake is preloading the deck with material intended to preempt every possible question. This turns a 30-minute conversation into a 90-minute slog and buries the actual ask. Trust that a CFO who wants more detail on cost sensitivity will ask, and be prepared to turn to slide 47 when they do.

The follow-up matters more than the presentation

The last practical point: the presentation is a moment in a longer relationship. CFOs are much more likely to approve programmes led by people who have demonstrated they will follow up honestly with results, own the mistakes, and report on the leading indicators as they come in. That reputation is built over multiple business cases, not in a single conversation.

If you are presenting your first major AI case, the CFO is not just deciding on the case; they are calibrating on you. The best thing you can do for the next case is to over-deliver on the reporting rhythm on this one. The organisations that build durable AI programmes are the ones where finance and programme leadership are working from shared evidence, not competing narratives. That trust is worth much more than any single approved investment.