Traditional financial modelling assumes you make an investment, then live with it. Real options thinking assumes you make an investment that opens up choices, and the choices themselves have value. That distinction matters enormously for AI, because AI investments almost always come with embedded optionality that standard NPV ignores.

I want to be careful in this article. Real options is a real branch of finance, with rigorous mathematical foundations (Black-Scholes, binomial trees, all of that), and I do not want to pretend the full machinery is easy or that every AI team should be running formal option valuations. But the concepts underneath, the way of thinking about staged investment under uncertainty, are among the most useful mental models I have for AI programme design. Even without the maths, using them changes how you build business cases and how you defend them.

Why standard NPV underweights AI investments

The core problem with NPV for uncertain investments is that it treats the future as a single expected path. You make an investment, you project cash flows, you discount them, you get a number. The number does not reflect the fact that as reality unfolds, you will make choices: expand if things go well, hold if the picture is unclear, pivot if the assumptions turn out wrong, abandon if the evidence is bad.

Each of those choices has value. If your AI pilot returns terrible early results, being able to shut it down before spending the full budget is worth something. If it returns great results, being able to scale it before competitors catch up is worth something. Standard NPV does not put a number on either. It assumes you commit the full spend and take whatever return the cash flow model produces.

This bias particularly hurts AI investments because AI has three characteristics that amplify the value of flexibility. Outcomes are highly uncertain, which means the range of possible futures is wide. Investments can be staged, which means you can commit incrementally as uncertainty resolves. And the value of learning from early stages is often high, which means the information you gain at each stage is itself worth something.

The result is that a standard NPV calculation on an AI programme often looks worse than the programme actually is, because the flexibility to adapt is invisible in the model. This is one of the reasons that projects with negative first-pass NPVs sometimes get approved anyway (the sponsor intuits value the model does not capture) and one of the reasons other projects get approved on positive NPVs and then blow up (the model did not price the downside).

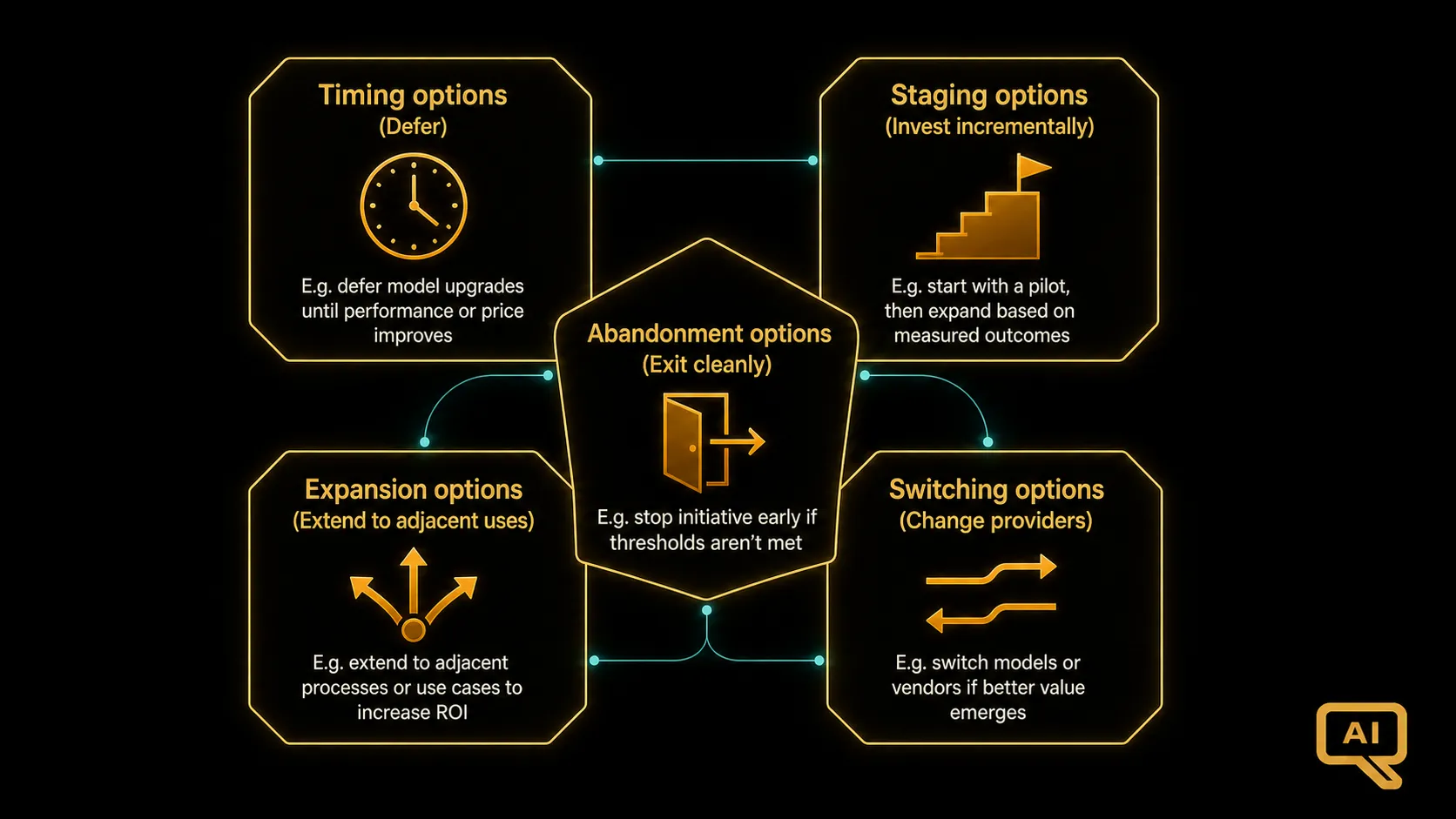

The five types of options in AI programmes

Figure 1 organises the five main types of real options as they apply to AI programmes. Each one shows up in almost every enterprise AI decision, whether or not it is being consciously modelled.

Timing options are the value of waiting. If you defer an investment, you learn more about the technology, prices, competitor moves, and regulation. The cost of waiting is the value of what you would have earned if you had started earlier. The benefit is the reduction in uncertainty. For rapidly evolving areas like agentic AI, the timing option is often large: waiting six months might save 40 percent on inference cost, resolve regulatory uncertainty, and give you access to a materially better model. Deferring is not always right, but it is not always wrong either, and the timing option deserves explicit consideration rather than being dismissed as inaction.

Staging options are the value of investing incrementally rather than all at once. A pilot is a stage. A controlled rollout is a stage. A full deployment is a stage. Each stage resolves some uncertainty and gives you the option to continue, expand, hold, or exit. The value of staging is huge when the underlying investment is uncertain, and it is much of what BCR-02’s milestone-and-gate structure is trying to capture.

Expansion options are the right to invest more if things go well. When you build an AI capability for one use case, you often create the potential to extend it to adjacent use cases at much lower incremental cost. That extensibility has real value even if you never exercise it, and the initial investment case should account for it.

Switching options are the right to change direction. Multi-model deployments create a switching option on the model provider. Modular architectures create a switching option on the underlying technology. Vendor abstraction creates a switching option on the platform. Each of these adds engineering complexity but preserves optionality when the landscape shifts.

Abandonment options, the fifth quadrant of Figure 1, are the right to stop. This sounds negative but it is one of the most valuable options in any uncertain investment. Being able to shut down a project after the pilot without wasting the deployment cost is worth real money, and the ability to do so cleanly is one of the most valuable investments you can make in your governance model.

The staged investment pattern

The most practical application of real options for AI programmes is staged investment with explicit go/no-go gates. This does not require Black-Scholes maths. It requires structuring the programme so that each stage has clear success criteria, and the decision to continue is separated from the decision to start.

A typical staged AI programme might look like this. Stage one is a bounded pilot with a defined use case, a small user cohort, and a fixed budget. The gate at the end asks: did we hit the success criteria on quality, adoption in the pilot cohort, and unit economics? Stage two is a controlled rollout to a larger group, with instrumentation to measure the effects. The gate asks: does the value hypothesis hold at scale, and is the cost per successful task in the expected range? Stage three is full deployment, with the confidence that comes from real production evidence.

Each stage has a smaller budget than committing the full programme upfront, and each stage produces information that either validates continuing or provides a clean exit point. The total programme cost, weighted by the probability of continuing at each gate, is typically much lower than the naive sum of all stages. That expected cost is what should go into the business case, not the maximum possible spend.

Structuring programmes this way is not just financial hygiene. It fundamentally changes what you can commit to. Rather than asking finance to underwrite a five-year programme, you are asking them to underwrite the first stage plus the option to continue. That is a much easier sale, and it aligns the risk profile with what is actually knowable.

The learning option

There is a class of AI investments where the primary return is not the direct P&L impact of the specific use case, but the organisational learning that comes from doing it. First-time deployments of RAG, first-time deployments of agents, first-time deployments in a new business domain: these often have modest direct returns, but the capability built through them enables faster and larger returns on subsequent investments.

Standard NPV misses this entirely. The direct return on the first project might not justify the cost, but the learning creates an option to do the second project much more cheaply and effectively. If your organisation is early in its AI journey, some proportion of your programme spend should be explicitly framed as buying options for the future, and the business case should say so rather than pretending the direct return is what justifies the investment.

Foundation model bets as options

At the extreme end of the option-thinking spectrum are the strategic bets. Committing to a foundation model provider before you know the full picture of the market. Building an agent platform before your use cases are fully defined. Establishing a partnership with a specific vendor before the vendor’s roadmap is settled.

These decisions are not well-modelled by NPV. They are options on the future evolution of the technology and the market. The value of the option depends on how much optionality it preserves, how quickly the underlying uncertainty resolves, and what the downside looks like if the bet turns out wrong.

The mistake I see most often is either taking these bets without acknowledging their option nature (leading to overcommitment on the basis of a spurious NPV), or refusing to take them because they cannot be justified on NPV (leading to strategic paralysis). Both failure modes come from applying the wrong framework. Option thinking gives you a language to evaluate these decisions on their actual terms.

When formal option valuation is worth doing

For most AI programmes, the option thinking is enough and the formal maths is overkill. But there are cases where a real options valuation is worth the effort. Very large investments where the flexibility value is a significant portion of the total. Situations where finance is genuinely undecided and needs a rigorous quantitative case for the option value. Comparisons between competing programmes with different option structures.

In those cases, the standard technique is a binomial tree or a Monte Carlo simulation that models the underlying uncertainty (usually the value of the investment at each stage) and the decision to continue or exit at each gate. The output is an expected value that includes the option value, which is often materially higher than the standard NPV.

The full mechanics of these techniques are covered in finance textbooks and are beyond the scope of this article. What matters here is knowing when to reach for them and being able to have a credible conversation with finance about the option value even when the maths itself is simplified.

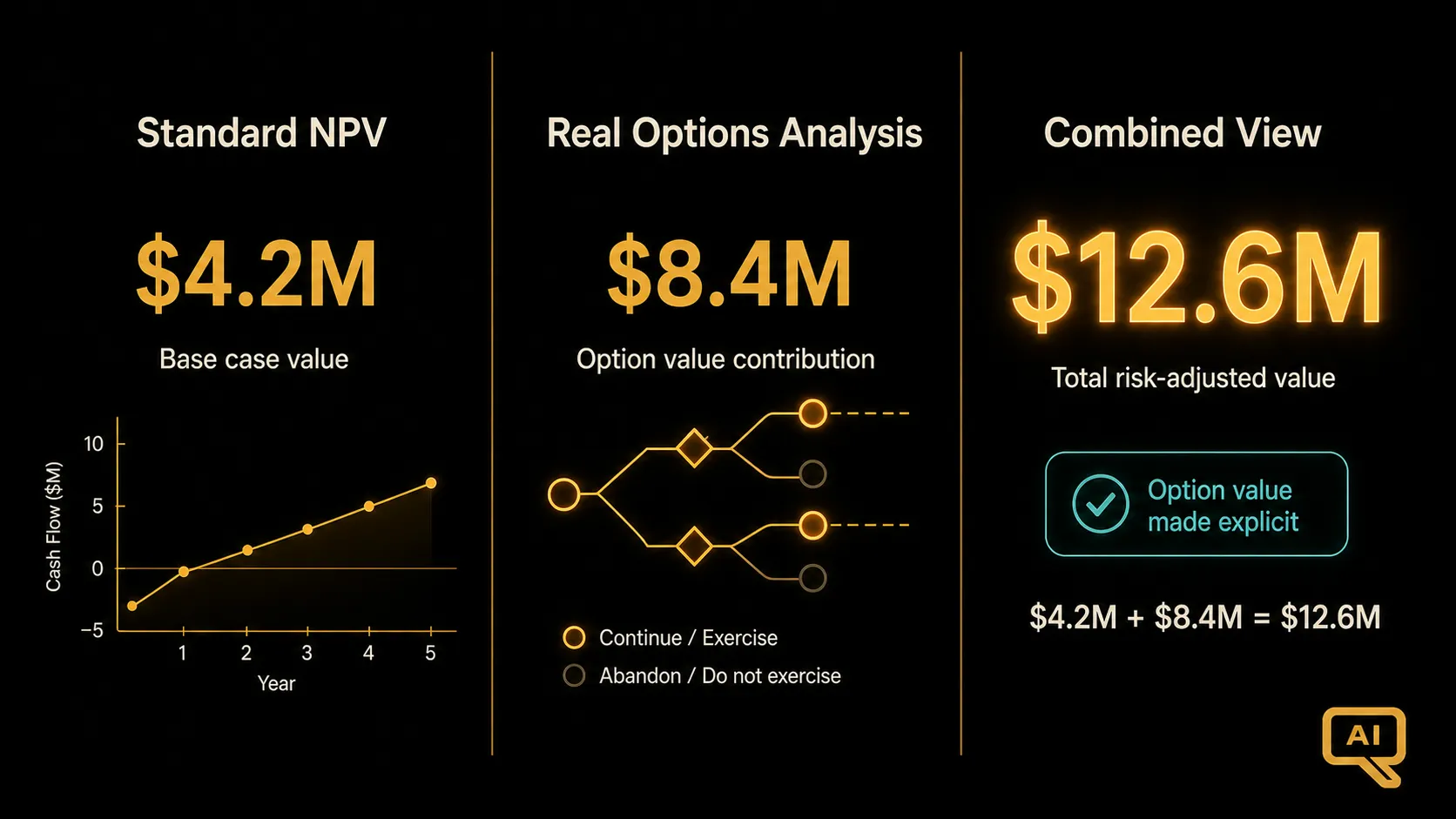

Combining NPV and real options in the business case

Figure 2 shows how I typically present the two frameworks together. Standard NPV is the base case: what is the investment worth on its expected cash flows? Real options analysis is the adjustment: what is the additional value from the flexibility, staging, expansion, switching, and abandonment options?

The combined view in Figure 2 gives a richer picture than either framework alone. Finance gets to see the standard-form return they are used to evaluating, and they also get to see the value of the specific programme design choices (staged investment, multi-model architecture, extensible platform) that would otherwise be invisible.

The point of all of this is not to inflate business cases with fictitious option value. It is to make the actual value of the programme visible in the financial model, including the parts that standard NPV systematically underweights. For AI programmes, which are uniquely characterised by high uncertainty, staged execution, and rapid learning, that is often the difference between a case that gets funded and one that does not.

Batch 1 of this track ends here. In batch 2, I move from the frameworks for building the case to the discipline of measuring, attributing, and defending the value once the programme is running. That is where good financial modelling becomes good financial reality.