Vendor pricing in AI is a moving target. The published rates on any given day are only the surface of a much more complex negotiation. Enterprise agreements, ramp deals, model version transitions, commitment structures, and side arrangements all bend the actual paid price away from the sticker price, sometimes dramatically. Getting this right matters, because unlike traditional software (where negotiation moves the number by 10 to 30 percent), AI negotiation can move the effective per-unit cost by 3 to 10 times.

I want to walk through the pricing models, the negotiation levers, and the contract terms that actually matter, based on what I have watched succeed and fail in enterprise procurement conversations through 2025 and 2026.

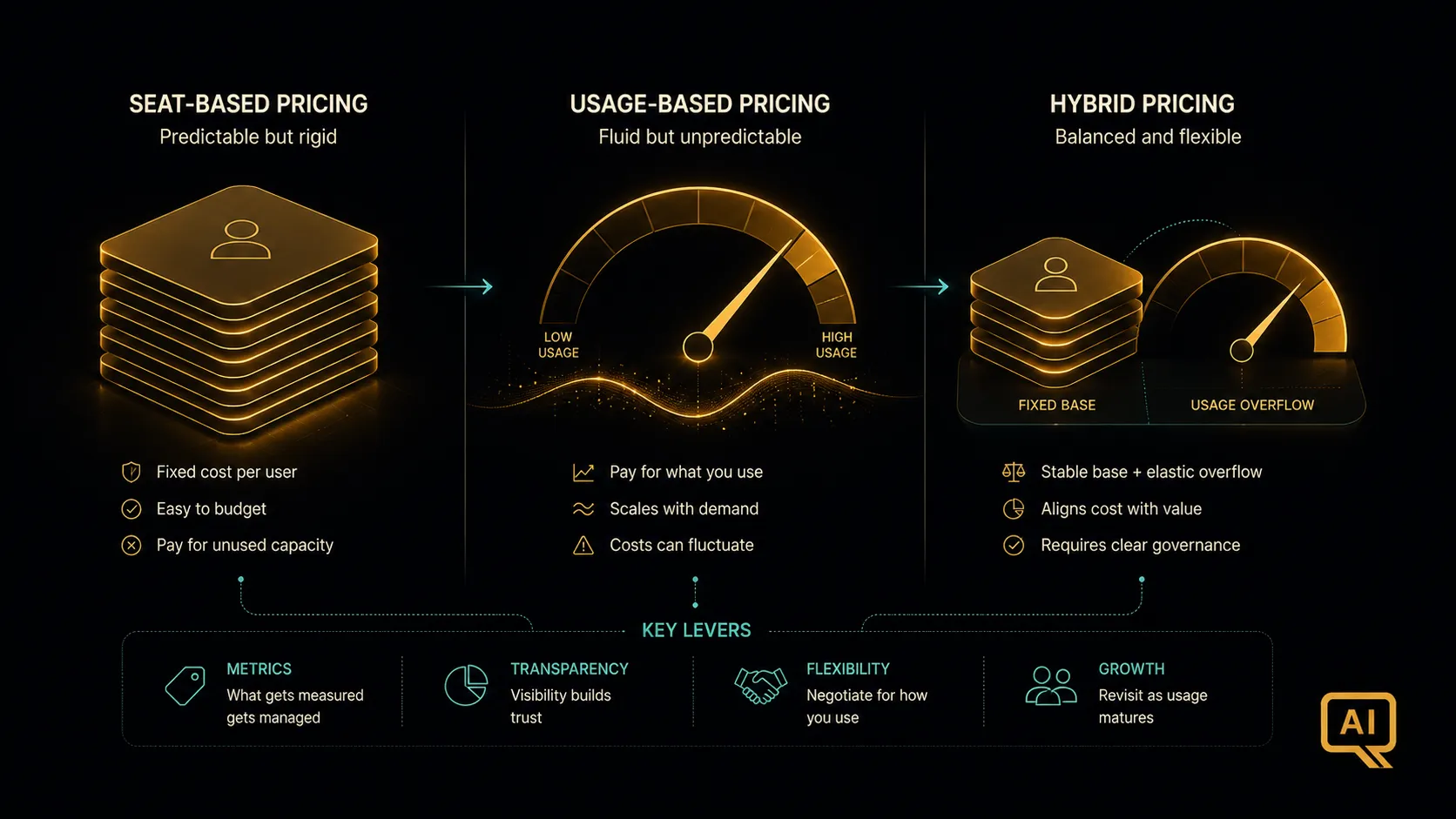

The four pricing model shapes

Enterprise AI vendors are currently pricing along four broad model shapes, and the shape matters more than the specific rate.

Seat-based pricing bills per user per month, typically for hosted assistants and copilots. Microsoft Copilot at $30/user/month, Claude Pro at $20/user/month, GitHub Copilot at similar rates. Seat-based is predictable, easy to budget, and hard to game. The trade-off is that you pay whether the user uses the tool heavily or barely at all, which means the effective cost per interaction varies enormously across your user base.

Usage-based pricing bills per token consumed, per API call, or per compute-second used. This is the dominant model for direct model access. Predictable at the unit level, unpredictable at the total-bill level, because usage scales with adoption in ways that can outrun the budget. This is where the Uber case happened.

Hybrid pricing combines seats and usage: a seat provides included capacity, and heavy users incur overage charges. This is where enterprise pricing is trending in 2026, because it captures the benefits of both models (budget predictability from the seat, cost fidelity from the overage).

Outcome-based pricing bills per successful task, per resolved case, or per business outcome. Rare in 2026 but growing. The pricing is much simpler on the customer side (“I paid $X and got Y successful outcomes”) but the vendor takes the risk of unpredictable unit economics on their side, which is why very few vendors offer this yet at scale.

The pricing games to watch for

Every vendor I have worked with runs at least a few of the following pricing games. Being alert to them is the first defence.

The high-tier upsell: pricing is skewed so that the “sensible” default is the higher tier, and the lower tier is deliberately limited in ways that push you to upgrade. Watch for context window caps, tool use limits, and quality tier restrictions on the base plan.

The model version reset: when the vendor releases a new model, existing customers often get migrated to the new pricing rather than grandfathered on the old. This can be a 20 to 50 percent effective cost increase overnight. It also happens the other way (new model at lower price for new customers, existing customers stuck at old price) and requires active management to capture the benefit.

The token accounting shift: Claude Opus 4.7 and later use a new tokenizer that produces roughly 30 percent more tokens for the same text. The per-token price is unchanged, but your effective bill goes up. Vendors often introduce these changes with minimal notice, and existing cost projections need to be revalidated.

The bundle pressure: usage discounts require committing to a broader bundle of services (compute, storage, other AI products from the same vendor). The unit rate is lower, but the total commitment locks you in.

The regional multiplier: as of 2026, Claude’s US-only inference option applies a 1.1x pricing multiplier. Similar patterns are appearing across other providers for data residency requirements. This adds real cost that is often overlooked at contract signing.

The reserved capacity pattern: heavy users can get 30 to 50 percent discounts by pre-committing to minimum consumption levels. The savings are real, but so is the risk of under-consuming the commit and paying for capacity you did not use.

The enterprise agreement structure that works

Figure 1 shows the shape of a well-structured enterprise AI agreement. Six elements matter, and each of them is negotiable.

The base commitment shown at the top of Figure 1 is the minimum you agree to spend, usually annually. Volume commitments unlock discount tiers. The trap is committing more than you will use; the opportunity is that the effective per-unit rate can drop dramatically at higher commits. Model the realistic usage range before signing, and commit at the low end of your projected range rather than the middle, so overage capture rather than commit shortfall is the failure mode.

The ramp period allows the commitment to grow over the contract term. Year one at a lower commit, year two higher, year three highest. This aligns with realistic adoption curves and gives you time to build usage without paying for capacity you cannot yet consume. Ramp deals are standard practice with mature enterprise vendors and should be part of any multi-year AI agreement.

Volume tiers define the price you pay at different consumption levels. Aggressive negotiation focuses on lowering the rate at your projected steady-state volume, not the rate at your entry-level volume. Vendors will often trade favourable steady-state rates for higher initial commits.

Price protection clauses lock in the negotiated rates against subsequent vendor price changes. Standard 12-month protection is common; 24 to 36 months is achievable with meaningful commitment. Without price protection, the vendor can raise the effective rate mid-contract and you have no recourse.

Deprecation notice requires the vendor to give minimum warning before deprecating models you have built on. Without this, a model refresh can force you into an emergency migration. 6 to 12 months of notice is a reasonable target.

Exit provisions define how you get out. Data portability, gradual reduction rights, and cure periods for vendor failures all matter. The default exit terms in most vendor contracts are punitive; negotiating them at signing is much easier than trying to negotiate them at exit.

The clauses that matter more than the price

Beyond the pricing structure, several contract clauses have outsized impact on total cost of ownership.

Data usage rights. Does the vendor train on your data by default? Can they? What is the process for opting out? What are the consequences if they do (retraining, extraction, disclosure)? These clauses matter for regulatory compliance and for competitive positioning; a vendor training on your data may be inadvertently sharing your insights with competitors.

Uptime service level agreements. AI provider outages happen, and the SLA determines your recourse. Standard SLAs offer credits against future service; enterprise agreements can negotiate meaningful downtime protection or contractual right to failover to competitor services.

Model behaviour guarantees. Can the vendor materially change the model behaviour under an existing model name without notice? Historically, the answer has been yes. Better contracts are starting to specify baseline evaluation performance the vendor must maintain, or notice periods for material behaviour changes.

Indemnification for outputs. If the model produces content that infringes copyright, defames a person, or violates regulation, who is liable? Vendor indemnification varies widely; enterprise agreements typically negotiate stronger vendor coverage than the default terms.

Support and access. Response times, dedicated account teams, technical escalation paths. For any AI deployment that touches production, these terms determine how you get help when the model does something unexpected at 2 AM.

The negotiation leverage you actually have

The mistake many AI procurement teams make is assuming they have no negotiating power, because the market is fast-growing and demand is high. That is only partly true. Enterprise AI vendors are competing for reference customers, high-visibility deployments, and predictable revenue commitments. You have leverage; the question is whether you use it.

The strongest leverage is architectural. Multi-model deployments (having a working alternative to your primary provider) fundamentally change the negotiation. A vendor that knows you can route workloads to their competitor within days will price and behave differently than a vendor that knows you are locked in. The engineering cost of maintaining multi-model capability is real, but it is often the highest-ROI negotiation investment you can make.

The second is data. Being able to characterise your actual workload precisely (tokens by tier, cache hit rate, request patterns, projected growth) makes you a much more credible negotiator than a customer waving a vague spend number around. Vendors offer better rates to customers they can price accurately.

The third is timing. AI vendor pricing has been changing every 3 to 6 months for two years. Contracts signed at one point in the pricing cycle can be dramatically different from contracts signed a few months later. Timing negotiations to coincide with vendor pricing updates, competitive launches, or quarter-end pressure is worth doing.

The fourth is reference value. Vendors regularly trade discounts for public reference customer status, case studies, or joint marketing. If you are willing to be visible, ask for it in the deal.

Watching for “agent washing” and vaporware

Figure 2 shows the evaluation checklist I use for AI vendor selection, because the fastest-growing category of business case failure in 2026 is vendors who overclaimed and underdelivered. Gartner has been calling this “agent washing” throughout 2026: rebranding non-agentic products as agents to ride the market cycle.

Running through the checklist in Figure 2, the specific red flags to watch for:

Vendors who cannot name three named customers currently in production and willing to take a reference call. “Strategic partnerships” and “pilot deployments” are not production references.

Demos that will not run against your data. If the vendor’s demo works only on their curated examples, you have no way to know how it will perform on your actual workloads.

ROI claims without underlying case studies. “Customers see 3x return” is not a data point; it is a marketing statement. Ask for the specific customer, the specific measurement, the specific timeframe, and the specific methodology.

Pricing that only holds at low volume. Enterprise pricing often gets worse as you scale, not better, because the vendor has to actually cover their cost of goods sold. Model the pricing at your projected scale, not at pilot scale.

Vendor viability signals. AI infrastructure spend at scale requires vendors to actually be well-funded and profitable enough to be around in 3 to 5 years. A vendor whose economics do not work at scale will either raise prices, restrict features, or go out of business, and each of those outcomes has real cost to you.

Building the vendor decision into the business case

The vendor decision belongs in the business case, not adjacent to it. Different vendors produce different economics, different capabilities, and different risk profiles, and the case should show which vendor you are underwriting and why.

The strongest business cases include a specific vendor comparison, the negotiated terms assumed for the primary vendor, the contingency plan if the primary vendor changes pricing or capabilities, and the total cost projection under both base case and downside scenarios. This may sound like extra work, but it is the difference between a business case that survives a vendor pricing shift and one that has to be rewritten every time the market moves.

The AI vendor landscape will continue to evolve rapidly. Building your programme to be resilient to that evolution, rather than dependent on any single vendor’s roadmap, is one of the most valuable architectural investments you can make. The negotiation is where that resilience gets encoded into the actual contract.